Okay, here’s a comprehensive article on Explanation of Benefits (EOB) statements, designed to meet your specifications. I’ve aimed for clear, informative content with a professional tone.

On this special occasion, we will be happy to review interesting topics related to insurance eob. Let’s weave interesting information and provide new views to readers.

Understanding Your Insurance Explanation of Benefits (EOB): A Comprehensive Guide

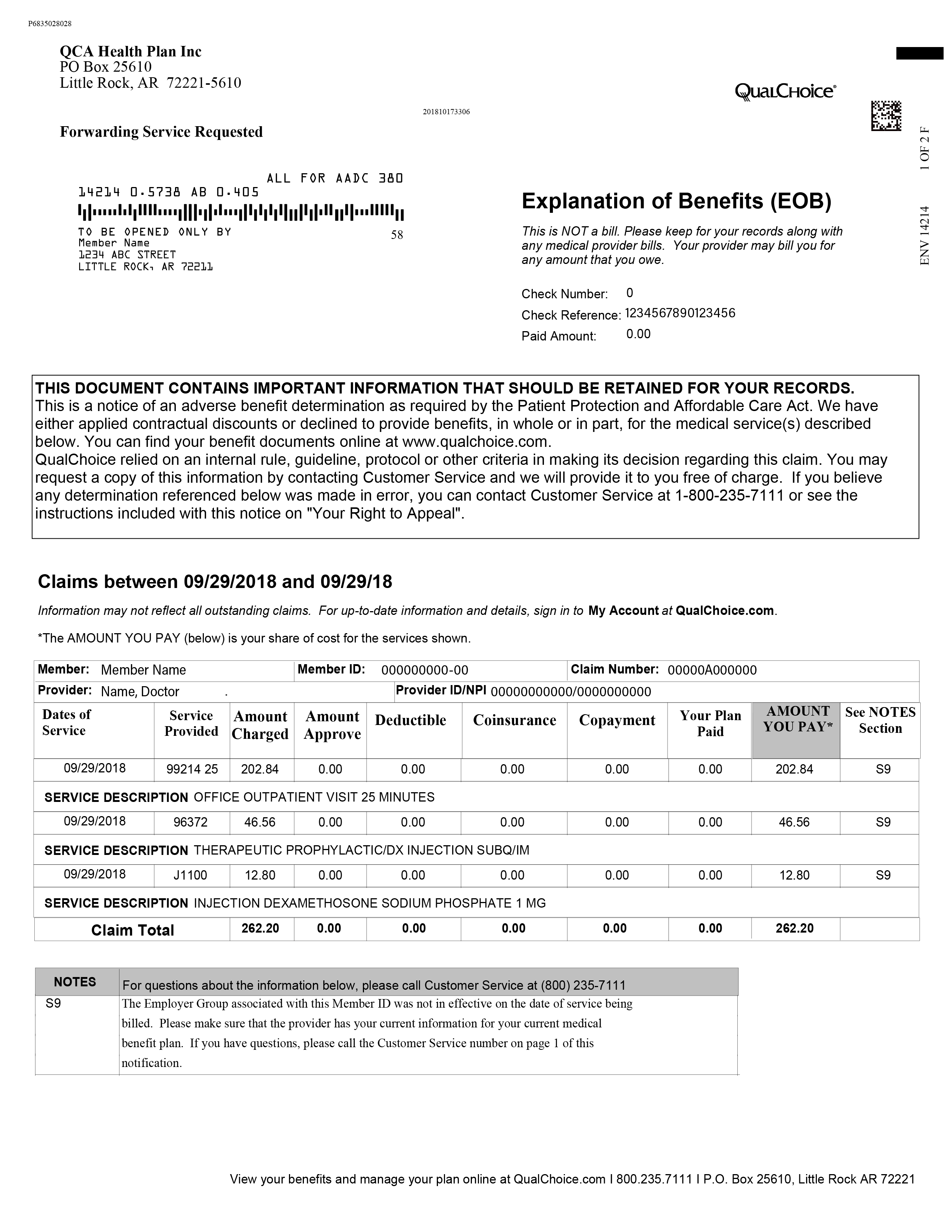

Navigating the complexities of health insurance can often feel like deciphering a foreign language. Between premiums, deductibles, copays, and coinsurance, understanding the financial implications of your healthcare can be daunting. One crucial document that helps demystify this process is the Explanation of Benefits, or EOB. While it may resemble a bill, the EOB is not a bill. It’s a detailed statement from your insurance company explaining how a medical claim was processed and what portion of the costs, if any, you are responsible for. Understanding your EOB is essential for ensuring accurate billing, tracking your healthcare spending, and identifying potential errors.

The Explanation of Benefits (EOB) serves as a bridge between your healthcare provider and your insurance company. After you receive medical services, your provider submits a claim to your insurance company for reimbursement. The insurance company then reviews the claim based on your policy’s coverage, deductible, copay, and coinsurance terms. The EOB is the insurance company’s response to that claim, outlining what they paid to the provider and what, if anything, you owe. Think of it as a report card for your medical claim, showing you exactly how your insurance benefits were applied.

One of the primary reasons to carefully review your EOB is to ensure accuracy. Errors in medical billing are more common than many people realize. These errors can range from incorrect coding of procedures to duplicate billing or even charges for services you didn’t receive. By scrutinizing your EOB, you can identify discrepancies and take steps to correct them. This could involve contacting your healthcare provider to verify the charges or disputing the claim with your insurance company. Catching these errors can save you money and prevent potential billing issues in the future.

The EOB also helps you track your progress towards meeting your deductible and out-of-pocket maximum. Your deductible is the amount you must pay for covered healthcare services before your insurance company starts to pay. The EOB will show you how much of your deductible has been met with each claim. Similarly, your out-of-pocket maximum is the most you’ll have to pay for covered services in a plan year. Once you reach this limit, your insurance company pays 100% of covered costs. Tracking these amounts on your EOBs allows you to anticipate future healthcare expenses and budget accordingly.

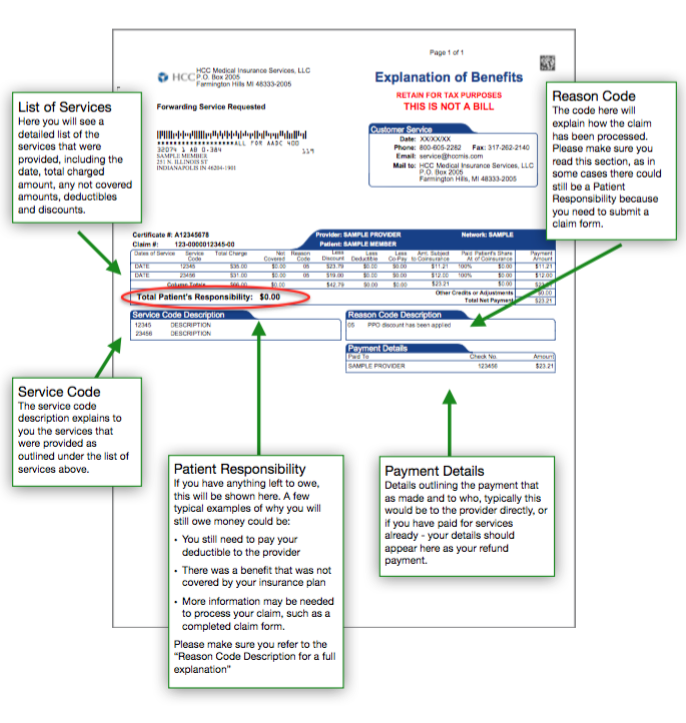

Understanding the specific components of an EOB is key to interpreting the information it contains. While the format may vary slightly depending on the insurance company, most EOBs include several essential elements. These elements typically include the patient’s name and policy number, the date of service, the name of the healthcare provider, a detailed description of the services provided, the amount billed by the provider, the amount the insurance company allowed, the amount the insurance company paid, and the patient’s responsibility.

The "Amount Billed" represents the original charge submitted by the healthcare provider for the services rendered. This is often not the amount you will ultimately pay, as insurance companies typically negotiate lower rates with providers. The "Amount Allowed" is the agreed-upon rate between the insurance company and the provider for the specific service. This is the maximum amount the insurance company will consider for payment. This difference between the amount billed and the amount allowed is often referred to as a "contractual adjustment" or "write-off," and you are not responsible for paying this difference.

The "Amount Paid" is the portion of the allowed amount that the insurance company covered based on your policy’s terms, including your deductible, copay, and coinsurance. This amount will reflect any applicable discounts or negotiated rates. The "Patient Responsibility" is the amount you are responsible for paying to the healthcare provider. This may include your copay, coinsurance, or any portion of the allowed amount that hasn’t been met by your deductible. This is the amount you should expect to see on your bill from the provider.

It’s important to understand the difference between a copay, coinsurance, and deductible. A copay is a fixed amount you pay for a specific service, such as a doctor’s visit or prescription. Coinsurance is a percentage of the allowed amount that you are responsible for paying. For example, if your coinsurance is 20%, you’ll pay 20% of the allowed amount for covered services. As mentioned earlier, the deductible is the amount you must pay out-of-pocket before your insurance company starts to pay for covered services.

One common point of confusion is understanding why you might owe money even after your insurance company has paid a portion of the bill. This is often due to unmet deductibles, coinsurance, or services that are not covered by your policy. For example, if you haven’t met your deductible, you’ll be responsible for paying the full allowed amount until you reach your deductible. Similarly, if your policy has a coinsurance provision, you’ll be responsible for paying your share of the allowed amount, even after your insurance company has paid their portion.

Another crucial aspect of reviewing your EOB is to verify that the services listed are actually the services you received. Compare the dates of service, the providers listed, and the descriptions of the services to your own records. If you notice any discrepancies, such as services you didn’t receive or incorrect dates, contact your healthcare provider and your insurance company immediately to investigate. Addressing these discrepancies promptly can prevent inaccurate billing and potential fraud.

If you disagree with the way your insurance company processed your claim, you have the right to appeal their decision. The EOB will typically include information on how to file an appeal, including the deadline for submitting your appeal and the required documentation. When filing an appeal, be sure to clearly state the reasons for your disagreement and provide any supporting documentation, such as medical records or a letter from your doctor.

Many insurance companies offer online portals where you can access your EOBs electronically. This can be a convenient way to track your healthcare spending and access your EOBs anytime, anywhere. Electronic EOBs are often more secure and environmentally friendly than paper statements. Check with your insurance company to see if they offer an online portal and how to access your EOBs electronically.

In addition to the information provided on the EOB, your insurance company may also include additional details or explanations in a separate section or attachment. This information may include details about the specific codes used to bill for the services, explanations of any denials or reductions in payment, or information about your rights as a policyholder. Be sure to review this additional information carefully to fully understand your EOB.

It’s also a good idea to keep your EOBs organized for your records. This can be helpful for tracking your healthcare spending, preparing your taxes, and resolving any billing disputes. You can either keep paper copies of your EOBs or save them electronically. Consider creating a filing system that makes it easy to find your EOBs when you need them.

Ultimately, understanding your Explanation of Benefits is a critical step in managing your healthcare costs and ensuring accurate billing. By carefully reviewing your EOBs, you can identify errors, track your progress towards meeting your deductible and out-of-pocket maximum, and ensure that you are only paying for the services you actually received. Take the time to familiarize yourself with the components of your EOB and don’t hesitate to contact your insurance company or healthcare provider if you have any questions or concerns.

Frequently Asked Questions (FAQs)

1. What is the difference between an EOB and a medical bill?

An EOB is a statement from your insurance company explaining how a medical claim was processed. It is not a bill. A medical bill comes directly from your healthcare provider and indicates the amount you owe them for services rendered. The EOB tells you what portion of that bill your insurance covered and what portion, if any, you are responsible for.

2. What should I do if I find an error on my EOB?

If you find an error on your EOB, such as incorrect services listed or inaccurate charges, contact both your healthcare provider and your insurance company immediately. Start by contacting your provider to verify the charges and ensure that the services listed are accurate. Then, contact your insurance company to dispute the claim and provide them with any supporting documentation.

3. My EOB says "Not Covered." What does that mean?

"Not Covered" means that your insurance policy does not cover the specific service you received. This could be because the service is not included in your policy’s coverage, or because you have not met your deductible, or because the service was deemed medically unnecessary. Contact your insurance company to understand why the service was not covered and explore your options for appealing the decision or seeking alternative treatments.

4. How long should I keep my EOBs?

It’s generally recommended to keep your EOBs for at least one year, or longer if you have complex medical conditions or ongoing billing disputes. Some experts recommend keeping them for up to three years, as this is the typical statute of limitations for medical debt. Keeping your EOBs organized can be helpful for tracking your healthcare spending, preparing your taxes, and resolving any billing issues.

5. Where can I find my EOBs?

Many insurance companies offer online portals where you can access your EOBs electronically. Check with your insurance company to see if they offer an online portal and how to access your EOBs. You may also receive paper EOBs in the mail. If you’re not receiving EOBs, contact your insurance company to ensure that they have your correct mailing address and email address.

Related Article

- Insurance For Life: Securing Your Future And Protecting Your Loved Ones

- Navigating The Healthcare Maze: A Comprehensive Look At Health Insurance Companies

- Navigating The World Of HMO Insurance: A Comprehensive Guide

- Insurance 25/50/25

- The Guardian Of Risk: A Deep Dive Into The World Of Insurance Underwriting

Thus, we hope this article has provided valuable insight into insurance eob. We thank you for your attention to our article. See you in our next article!