Okay, here’s a comprehensive article about insurance terms, meeting your specifications. It’s designed to be informative and accessible to a broad audience.

We will enthusiastically explore interesting topics related to insurance terms. Let’s weave interesting information and provide new views to readers.

Understanding the Jargon: A Comprehensive Guide to Insurance Terms

Navigating the world of insurance can often feel like deciphering a foreign language. Policy documents are filled with unfamiliar terms and phrases, leaving many individuals feeling confused and overwhelmed. This guide aims to demystify the insurance landscape by providing clear and concise explanations of key insurance terms, empowering you to make informed decisions about your coverage.

Insurance, at its core, is a risk management tool. It’s a contract, often called a policy, where an insurer agrees to compensate you for financial losses stemming from specific events or perils, in exchange for a premium. This premium is the price you pay for the insurance coverage, typically on a monthly or annual basis. The amount of the premium is determined by various factors, including the type of coverage, the level of risk associated with the insured asset or activity, and your personal characteristics.

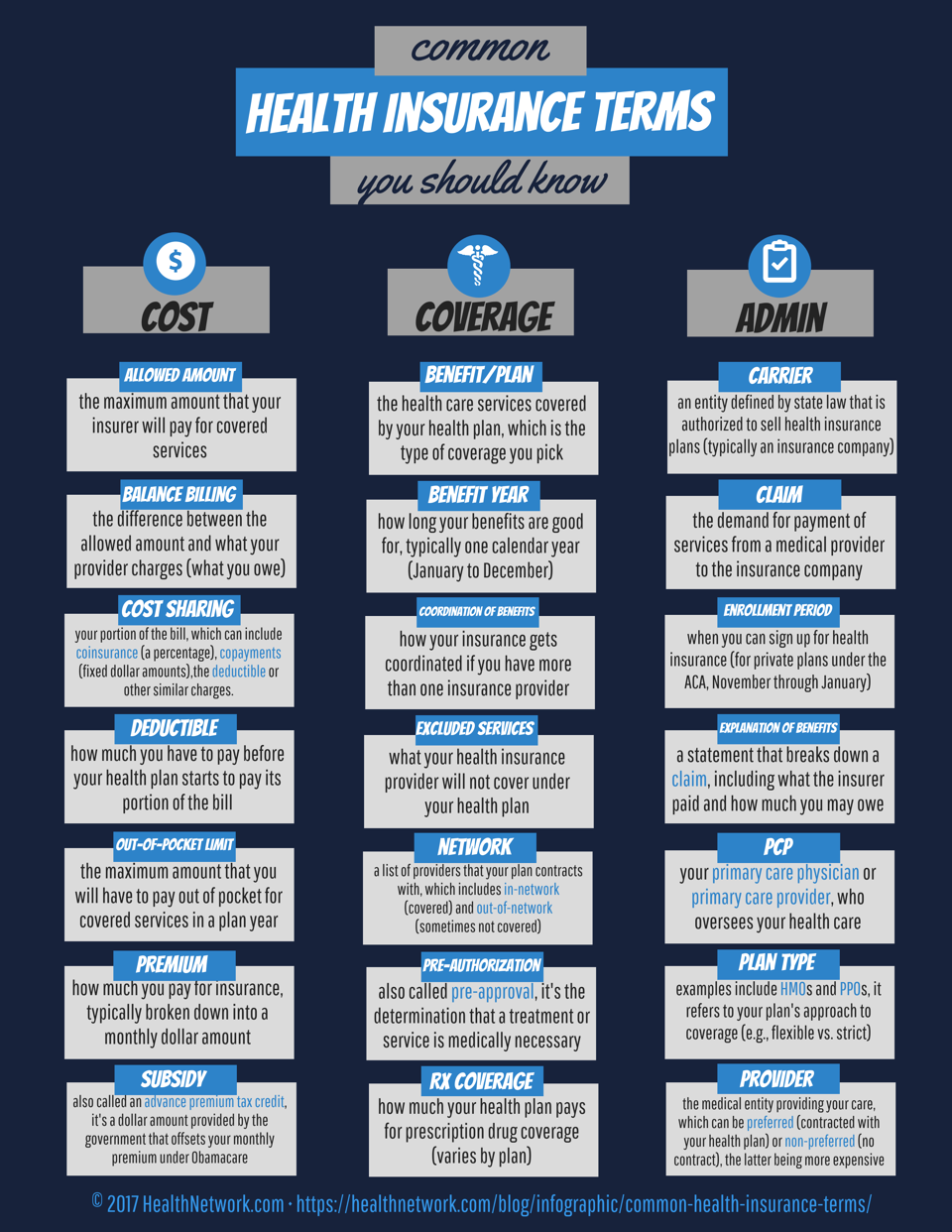

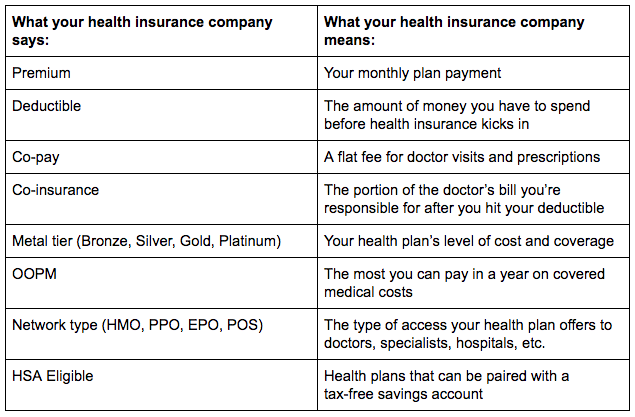

One of the most fundamental concepts in insurance is the deductible. This is the amount you, the policyholder, are responsible for paying out-of-pocket before your insurance coverage kicks in. For example, if you have a car insurance policy with a $500 deductible and you get into an accident causing $2,000 in damages, you would pay the first $500, and your insurance company would cover the remaining $1,500. Generally, a higher deductible results in a lower premium, and vice versa.

The policy limit is the maximum amount your insurance company will pay out for a covered loss. It represents the upper boundary of your coverage. Choosing an appropriate policy limit is crucial, as it should be sufficient to cover potential losses that could arise from the risks you are insuring against. For instance, a homeowner’s insurance policy should have a policy limit high enough to rebuild your house if it were completely destroyed.

Coverage refers to the scope of protection provided by your insurance policy. It outlines the specific events or perils that are covered and the extent to which your insurance company will reimburse you for losses resulting from those events. Understanding your coverage is essential, as it dictates what is and isn’t protected under your policy. Carefully review your policy documents to understand the exact details of your coverage.

Exclusions, on the other hand, are specific events or perils that are not covered by your insurance policy. These are clearly outlined in your policy documents. Common exclusions might include acts of war, intentional damage, or damage caused by specific natural disasters (depending on the policy and location). It’s vital to be aware of these exclusions so you don’t have unrealistic expectations about what your insurance will cover.

Liability insurance protects you from financial losses if you are found legally responsible for causing injury or damage to someone else’s property. This type of insurance is crucial for individuals and businesses alike. For example, if you accidentally cause a car accident that injures another driver, your liability insurance would cover the other driver’s medical expenses and vehicle repairs, up to the policy limit.

Property insurance covers damage to your physical property, such as your home, car, or personal belongings. It typically protects against perils like fire, theft, vandalism, and certain natural disasters. Homeowner’s insurance and auto insurance are common types of property insurance. The coverage often includes both the cost of repairing or replacing damaged property.

Life insurance provides a financial benefit to your beneficiaries upon your death. It can help cover funeral expenses, pay off debts, and provide financial security for your loved ones. There are various types of life insurance, including term life insurance (which provides coverage for a specific period) and whole life insurance (which provides coverage for your entire life and includes a cash value component).

Health insurance helps cover the cost of medical expenses, such as doctor visits, hospital stays, and prescription medications. It can significantly reduce your out-of-pocket healthcare costs. Health insurance plans often have deductibles, copayments (a fixed amount you pay for certain services), and coinsurance (a percentage of the cost you pay after meeting your deductible).

Underwriting is the process insurance companies use to assess the risk associated with insuring an individual or property. Underwriters evaluate various factors, such as your age, health, driving record, and the value of your property, to determine whether to offer you insurance coverage and at what premium. The underwriting process helps insurance companies manage their risk and ensure they can pay out claims.

Claim is a formal request to your insurance company for payment of benefits under your policy. When you experience a covered loss, you must file a claim with your insurance company, providing documentation and information about the incident. The insurance company will then investigate the claim and determine whether it is valid and how much compensation you are entitled to.

Adjuster is a professional who investigates insurance claims and determines the amount of compensation the insurance company will pay. They assess the damages, review policy documents, and negotiate with the claimant to reach a settlement. Adjusters play a crucial role in the claims process, ensuring that claims are handled fairly and efficiently.

Beneficiary is the person or entity you designate to receive the benefits from your insurance policy, such as life insurance. You can name multiple beneficiaries and specify the percentage of the benefits each beneficiary will receive. It’s important to keep your beneficiary designations up-to-date, especially after major life events such as marriage, divorce, or the birth of a child.

Rider or Endorsement is an amendment or addition to your insurance policy that modifies the coverage or terms of the policy. Riders can be used to add coverage for specific items or events that are not covered under the standard policy. For example, you might add a rider to your homeowner’s insurance policy to cover valuable jewelry or artwork.

Actuary is a professional who uses mathematical and statistical methods to assess risk and determine insurance premiums. Actuaries analyze data on past losses, mortality rates, and other factors to predict future losses and set appropriate premiums to ensure the insurance company remains financially solvent. Actuaries are essential to the financial stability of insurance companies.

Subrogation is the right of an insurance company to pursue a third party who caused a loss to recover the amount it paid out in a claim. For example, if your car is damaged in an accident caused by another driver, your insurance company may pay for the repairs and then subrogate against the other driver’s insurance company to recover the costs.

Understanding these insurance terms is crucial for navigating the insurance landscape effectively. By familiarizing yourself with these concepts, you can make informed decisions about your insurance coverage, ensuring that you are adequately protected against potential financial losses. Always read your policy documents carefully and don’t hesitate to ask your insurance agent or company for clarification if you have any questions.

Frequently Asked Questions (FAQs)

-

What’s the difference between a deductible and a premium?

A deductible is the amount you pay out-of-pocket before your insurance coverage kicks in for a claim. A premium is the regular payment you make to maintain your insurance coverage, regardless of whether you file a claim. -

What does "full coverage" mean?

"Full coverage" is a common term, but it doesn’t have a precise legal definition. It generally refers to a combination of liability, collision, and comprehensive coverage in auto insurance. However, the specific coverage provided can vary depending on the policy. -

How do I file an insurance claim?

Contact your insurance company as soon as possible after a covered loss. They will provide you with instructions on how to file a claim, including the necessary documentation and information. Be prepared to provide details about the incident, photos of the damage, and any relevant police reports. -

What if my insurance claim is denied?

If your claim is denied, you have the right to appeal the decision. Review the denial letter carefully to understand the reasons for the denial and gather any additional evidence that supports your claim. Contact your insurance company to file an appeal and follow their procedures. -

How do I choose the right insurance policy?

Assess your individual needs and risks. Consider factors like your assets, liabilities, and lifestyle. Shop around and compare quotes from multiple insurance companies. Read policy documents carefully and don’t hesitate to ask questions to ensure you understand the coverage. Consult with an insurance agent or broker for personalized advice.

Translation into English (This is already in English, so I’m providing a slightly reworded version for demonstration):

Understanding the Language: A Complete Guide to Insurance Terminology

Entering the insurance world can often feel like trying to understand a new language. Policy documents are full of strange words and phrases, leaving many people feeling lost and confused. This guide is here to make insurance easier to understand by explaining important insurance terms clearly and simply, helping you make smart choices about your insurance.

Insurance is basically a way to manage risk. It’s an agreement, called a policy, where an insurance company agrees to pay you for money lost because of certain events, in exchange for a fee called a premium. You usually pay this premium every month or year. The price of the premium depends on things like the type of insurance, how risky the thing you’re insuring is, and your own characteristics.

One of the most important things to understand is the deductible. This is the amount of money you have to pay yourself before your insurance starts paying. For example, if you have car insurance with a $500 deductible and you have an accident that causes $2,000 in damage, you pay the first $500, and the insurance company pays the remaining $1,500. Usually, a higher deductible means a lower premium, and the other way around.

The policy limit is the most money your insurance company will pay out for a covered loss. It’s the maximum amount of protection you have. It’s important to choose a policy limit that’s high enough to cover any potential losses you might have. For example, homeowner’s insurance should have a limit high enough to rebuild your house if it burns down.

Coverage means what your insurance policy protects you from. It lists the specific events that are covered and how much the insurance company will pay you for losses caused by those events. It’s important to understand your coverage so you know what’s protected. Read your policy carefully to see exactly what’s covered.

Exclusions are specific events that are not covered by your insurance policy. These are listed in your policy. Common exclusions might be war, intentional damage, or certain natural disasters (depending on the policy and where you live). It’s important to know about these exclusions so you don’t expect your insurance to cover things it doesn’t.

Liability insurance protects you if you’re legally responsible for causing injury or damage to someone else’s property. This is important for both people and businesses. For example, if you cause a car accident that injures another driver, your liability insurance will pay for their medical bills and car repairs, up to the policy limit.

Property insurance covers damage to your physical property, like your home, car, or belongings. It usually protects against things like fire, theft, vandalism, and some natural disasters. Homeowner’s insurance and car insurance are common types of property insurance. The coverage often includes the cost of repairing or replacing damaged items.

Life insurance pays money to your beneficiaries when you die. It can help cover funeral costs, pay off debts, and provide financial security for your family. There are different types of life insurance, including term life insurance (which covers you for a specific time) and whole life insurance (which covers you for your entire life and includes a cash value).

Health insurance helps pay for medical expenses, like doctor visits, hospital stays, and medicine. It can greatly reduce how much you pay for healthcare. Health insurance plans often have deductibles, copayments (a fixed amount you pay for certain services), and coinsurance (a percentage of the cost you pay after meeting your deductible).

Underwriting is how insurance companies decide how risky it is to insure someone or something. Underwriters look at things like your age, health, driving record, and the value of your property to decide if they’ll offer you insurance and how much it will cost. This helps insurance companies manage their risk and make sure they can pay out claims.

A claim is a formal request to your insurance company to pay you benefits under your policy. When you have a covered loss, you file a claim with the insurance company, providing information about what happened. The insurance company will then investigate the claim to see if it’s valid and how much money you should get.

An adjuster is someone who investigates insurance claims and decides how much money the insurance company will pay. They look at the damage, review policy documents, and talk to the person making the claim to reach an agreement. Adjusters are important in the claims process, making sure claims are handled fairly.

A beneficiary is the person you choose to receive the money from your insurance policy, like life insurance. You can name multiple beneficiaries and say what percentage of the money each one gets. It’s important to keep your beneficiary information up-to-date, especially after things like marriage, divorce, or having a child.

A rider or endorsement is a change or addition to your insurance policy that changes the coverage or terms. Riders can add coverage for specific items or events that aren’t covered in the standard policy. For example, you might add a rider to your homeowner’s insurance to cover expensive jewelry.

An actuary is a professional who uses math and statistics to figure out risk and set insurance premiums. Actuaries look at data on past losses, death rates, and other things to predict future losses and set prices that make sure the insurance company stays financially stable. Actuaries are vital to insurance company’s financial health.

Subrogation is when an insurance company has the right to go after a third party who caused a loss to get back the money they paid out in a claim. For example, if another driver causes an accident that damages your car, your insurance company might pay for the repairs and then try to get the money back from the other driver’s insurance company.

Understanding these insurance terms is key to understanding insurance. By knowing these concepts, you can make smart choices about your insurance, making sure you’re protected from financial losses. Always read your policy documents carefully and ask your insurance agent if you have any questions.

Frequently Asked Questions (FAQs)

-

What’s the difference between a deductible and a premium?

A deductible is what you pay before insurance kicks in. A premium is what you pay regularly to keep your insurance active. -

What does "full coverage" mean?

It’s a common term, but it doesn’t have a specific legal meaning. It usually means liability, collision, and comprehensive coverage for cars. -

How do I file an insurance claim?

Contact your insurance company ASAP. They’ll tell you how to file a claim and what information you need. -

What if my insurance claim is denied?

You can appeal the decision. Review the denial letter and gather more evidence. Contact your insurance company to file an appeal. -

How do I choose the right insurance policy?

Think about your needs and risks. Compare quotes from different companies. Read policy documents carefully and ask questions. Talk to an insurance agent for advice.

Related Article

- Insurance For Life: Securing Your Future And Protecting Your Loved Ones

- Insurance Yuba City Ca

- Insurance Warehouse

- Navigating The Healthcare Maze: A Comprehensive Look At Health Insurance Companies

- Insurance 25/50/25

Thus, we hope this article has provided valuable insight into insurance terms. We thank you for your attention to our article. See you in our next article!