The 80% Rule in Home Insurance: Understanding Coinsurance and Protecting Your Investment

On this special occasion, we will be happy to review interesting topics related to The 80% Rule in Home Insurance: Understanding Coinsurance and Protecting Your Investment. Come on weave interesting information and provide new views to readers.

Homeownership is a significant investment, and protecting that investment is paramount. Home insurance policies are designed to provide that crucial financial safety net, shielding you from the devastating costs associated with fire, theft, natural disasters, and other covered perils. However, navigating the intricacies of home insurance can be daunting, especially when you encounter terms like "coinsurance" and the "80% rule." Understanding these concepts is vital to ensuring you have adequate coverage and avoid potentially costly financial surprises when filing a claim.

The 80% rule is a common clause in homeowner’s insurance policies that directly impacts the amount of coverage you receive in the event of a loss. It essentially stipulates that you must insure your home for at least 80% of its replacement cost to be fully covered for any covered loss, up to the policy limits. Replacement cost refers to the amount it would take to rebuild your home at today’s prices, using similar materials and construction methods. It’s crucial to understand that replacement cost is not the same as market value, which includes factors like land value and location.

Why does this rule exist? Insurance companies implement the 80% rule to encourage homeowners to maintain adequate coverage that accurately reflects the true cost of rebuilding their homes. If homeowners could insure their homes for significantly less than the replacement cost, they might be tempted to underinsure, leading to a situation where the insurance company wouldn’t have sufficient funds to cover a major loss affecting multiple properties simultaneously. The 80% rule ensures a more stable and predictable risk pool for the insurance company.

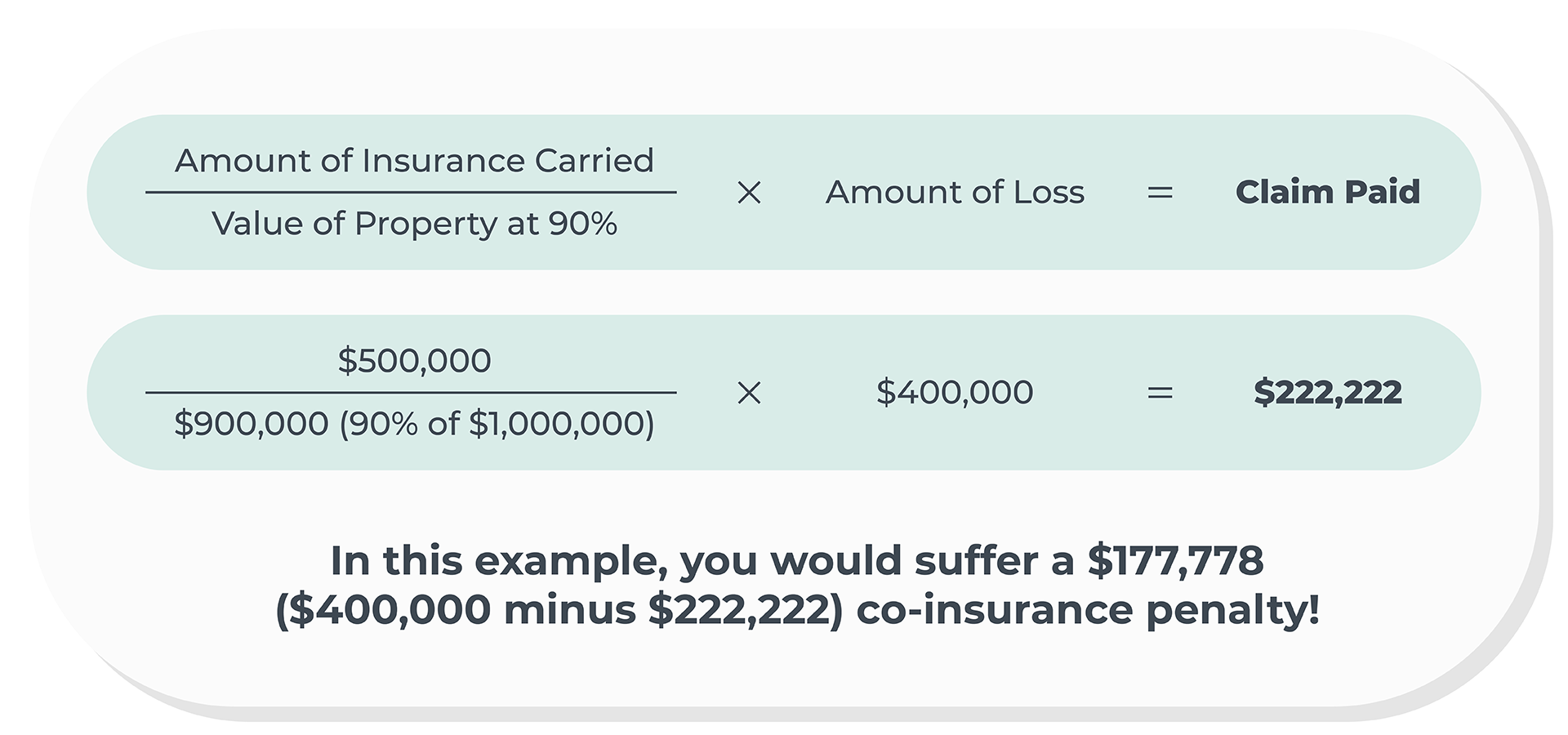

Failing to comply with the 80% rule can have significant financial consequences. If you insure your home for less than 80% of its replacement cost, you may face a penalty known as "coinsurance." Coinsurance means that you, as the homeowner, will share a portion of the loss with the insurance company. This portion is calculated based on the difference between the amount of insurance you carried and the amount you should have carried according to the 80% rule. In essence, you become a co-insurer of your own property.

Let’s illustrate this with an example. Imagine your home’s replacement cost is $500,000. To comply with the 80% rule, you need to insure it for at least $400,000 (80% of $500,000). However, you only insure it for $300,000. Now, let’s say a fire causes $100,000 in damage. Because you are underinsured, the insurance company will not pay the full $100,000. Instead, they will apply the coinsurance penalty.

The coinsurance penalty is calculated as follows: (Amount of Insurance Carried / Amount of Insurance Required) x Loss Amount. In our example, this would be ($300,000 / $400,000) x $100,000 = $75,000. This means the insurance company will only pay $75,000, and you will be responsible for the remaining $25,000. This significant out-of-pocket expense highlights the importance of adhering to the 80% rule.

The consequences of underinsurance can be even more devastating in the event of a total loss. If your home is completely destroyed and you are underinsured, the insurance company will only pay up to your policy limit, which is less than the actual cost to rebuild. This could leave you with a substantial financial shortfall, potentially forcing you to take out a loan or sell assets to cover the rebuilding expenses.

Determining the correct replacement cost of your home is crucial for complying with the 80% rule. While you can estimate it yourself, it’s highly recommended to consult with a qualified insurance professional or a professional appraiser. They can assess your home’s unique characteristics, including its size, construction materials, architectural style, and local labor costs, to provide a more accurate estimate.

Several factors can influence the replacement cost of your home. These include the size of your home (square footage), the quality of materials used in construction (e.g., brick, wood, siding), the architectural style (e.g., ranch, colonial, Victorian), the complexity of the design, any unique features (e.g., custom cabinetry, high-end appliances), and local labor costs. Fluctuations in the cost of building materials and labor can also impact the replacement cost over time.

It’s essential to review your home insurance policy annually, or even more frequently, to ensure that your coverage remains adequate. As your home ages, you may make improvements or renovations that increase its value and, consequently, its replacement cost. Similarly, changes in the local housing market and construction costs can also affect the replacement cost. Regularly updating your policy ensures that you are always adequately protected.

Beyond the 80% rule, consider purchasing Guaranteed Replacement Cost coverage. This endorsement provides even greater protection by covering the full cost of rebuilding your home, even if it exceeds your policy limits. This can be particularly beneficial in areas where construction costs have risen significantly or in situations where unexpected challenges arise during the rebuilding process.

Another valuable endorsement to consider is Extended Replacement Cost coverage. This option provides a buffer above your policy limits, typically 20% to 25%, to cover unexpected cost overruns during rebuilding. This can provide peace of mind knowing that you have additional financial protection in case of unforeseen circumstances.

When selecting a home insurance policy, don’t solely focus on the premium. While affordability is important, prioritize adequate coverage that complies with the 80% rule and considers your individual needs and circumstances. Consult with an independent insurance agent who can provide unbiased advice and help you compare policies from multiple insurers to find the best fit for your situation.

Understanding the 80% rule is a crucial step in protecting your home and your financial well-being. By ensuring you have adequate coverage, you can avoid potentially devastating financial losses in the event of a covered peril. Remember to regularly review your policy, consult with a qualified professional, and consider additional coverage options like Guaranteed or Extended Replacement Cost to provide even greater peace of mind. Taking these proactive steps will help you safeguard your most valuable asset – your home.

Finally, carefully read your insurance policy document. Pay close attention to the definitions of "replacement cost," "coinsurance," and any other relevant terms. If you have any questions or concerns, don’t hesitate to contact your insurance agent or company for clarification. Understanding the terms and conditions of your policy is essential for making informed decisions about your coverage and ensuring that you are adequately protected.

Frequently Asked Questions (FAQs)

1. What happens if I don’t comply with the 80% rule?

If you don’t comply with the 80% rule, you may face a coinsurance penalty. This means that the insurance company will only pay a portion of your claim, and you will be responsible for the remaining amount. The portion the insurance company pays is calculated based on the ratio of the insurance you carried to the insurance you should have carried according to the 80% rule.

2. How do I determine the replacement cost of my home?

You can estimate the replacement cost of your home yourself, but it’s best to consult with a qualified insurance professional or a professional appraiser. They can assess your home’s unique characteristics, including its size, construction materials, architectural style, and local labor costs, to provide a more accurate estimate.

3. Is the 80% rule the same as market value?

No, the 80% rule is based on the replacement cost of your home, which is the amount it would take to rebuild it at today’s prices. Market value includes factors like land value and location, which are not relevant to the cost of rebuilding.

4. What is Guaranteed Replacement Cost coverage?

Guaranteed Replacement Cost coverage is an endorsement that covers the full cost of rebuilding your home, even if it exceeds your policy limits. This provides extra protection in areas where construction costs are high or if unexpected challenges arise during rebuilding.

5. How often should I review my home insurance policy?

You should review your home insurance policy annually, or even more frequently, to ensure that your coverage remains adequate. Life changes, home improvements, and fluctuations in construction costs can all impact the replacement cost of your home and the adequacy of your coverage.

Related Article

- Navigating The World Of Insurance Breast Pumps: A Comprehensive Guide For Expecting And New Mothers

- Navigating The World Of HMO Insurance: A Comprehensive Guide

- The Guardian Of Risk: A Deep Dive Into The World Of Insurance Underwriting

- Insurance Yuba City Ca

- Insurance Warehouse

Thus, we hope this article has provided valuable insight into The 80% Rule in Home Insurance: Understanding Coinsurance and Protecting Your Investment. We hope you find this article informative and useful. See you in our next article!