Decoding the Out-of-Pocket Maximum: Your Shield Against Catastrophic Healthcare Costs

On this special occasion, we will be happy to review interesting topics related to Decoding the Out-of-Pocket Maximum: Your Shield Against Catastrophic Healthcare Costs. Come on weave interesting information and provide new views to readers.

Navigating the world of health insurance can feel like deciphering a complex code. Co-pays, deductibles, co-insurance, premiums – the terminology alone can be overwhelming. However, understanding these terms is crucial for managing your healthcare expenses and protecting your financial well-being. Among these crucial concepts, the "out-of-pocket maximum" stands out as a particularly important safeguard, acting as a financial shield against potentially crippling medical bills. This article aims to demystify the out-of-pocket maximum, exploring its function, its implications, and how it can significantly impact your healthcare spending.

The out-of-pocket maximum, often abbreviated as OOPM, is the absolute limit on the amount of money you will pay for covered healthcare services within a specific plan year. Think of it as a ceiling. Once you reach this limit, your insurance company will cover 100% of your eligible medical expenses for the remainder of that plan year. This provides crucial financial protection, especially in the event of a serious illness or injury requiring extensive and expensive treatment. Without an out-of-pocket maximum, you could potentially face unlimited medical debt.

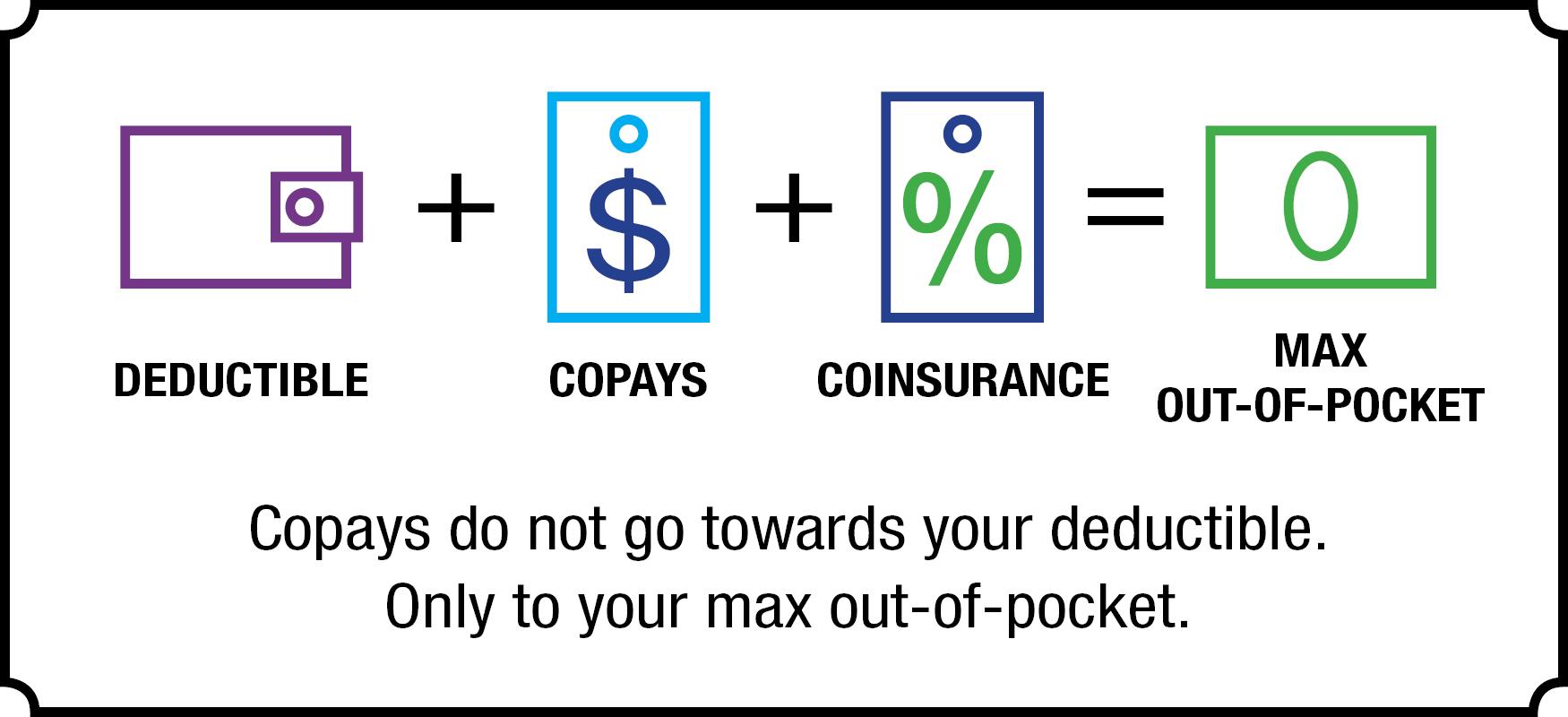

To fully grasp the significance of the out-of-pocket maximum, it’s essential to understand its relationship to other key insurance terms like deductibles, co-pays, and co-insurance. The deductible is the amount you pay for covered healthcare services before your insurance begins to pay. Co-pays are fixed amounts you pay for specific services, such as a doctor’s visit or prescription. Co-insurance is the percentage of the cost of covered services that you pay after you’ve met your deductible. All these expenses – deductibles, co-pays, and co-insurance – contribute towards your out-of-pocket maximum.

It’s important to note that not all healthcare expenses count towards your out-of-pocket maximum. Premiums, the monthly payments you make to maintain your insurance coverage, do not count towards your OOPM. Additionally, costs for services that are not covered by your plan, such as certain elective procedures or out-of-network care (unless it’s an emergency), will not contribute to reaching your maximum. Carefully review your insurance policy to understand which services are covered and which are not. This proactive approach can prevent unexpected and costly surprises.

The specific amount of your out-of-pocket maximum varies depending on your insurance plan. Plans with lower premiums often have higher out-of-pocket maximums, while plans with higher premiums tend to have lower maximums. Choosing the right plan involves carefully weighing these factors and considering your individual healthcare needs and risk tolerance. If you anticipate needing frequent medical care, a plan with a lower out-of-pocket maximum might be more beneficial, even if it means paying a higher monthly premium.

The Affordable Care Act (ACA) sets limits on the maximum out-of-pocket costs for marketplace plans. These limits are adjusted annually to reflect changes in healthcare costs. For 2024, the maximum out-of-pocket limit for an individual is $9,450, and for a family, it’s $18,900. These limits apply to most health insurance plans, including those offered through employers, the Health Insurance Marketplace, and Medicare Advantage. Understanding these limits provides a benchmark for evaluating the cost-effectiveness of different insurance options.

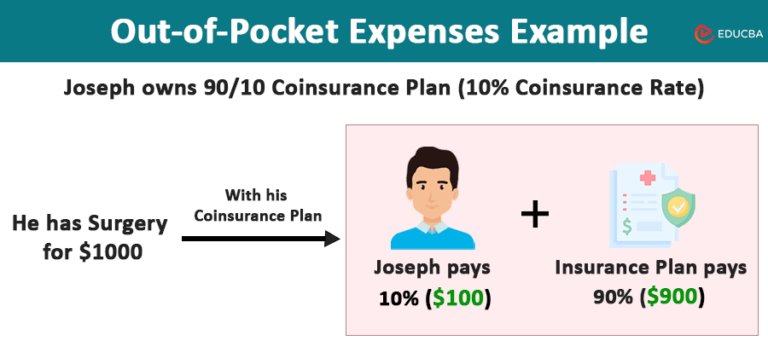

Consider this scenario: You have a health insurance plan with a $2,000 deductible, 20% co-insurance, and a $6,000 out-of-pocket maximum. You experience a medical emergency requiring hospitalization and extensive treatment, resulting in $30,000 in covered medical expenses. First, you would pay your $2,000 deductible. Then, you would pay 20% of the remaining $28,000, which amounts to $5,600. Your total out-of-pocket expenses would then be $2,000 (deductible) + $5,600 (co-insurance) = $7,600. However, since your out-of-pocket maximum is $6,000, you would only pay $6,000, and your insurance company would cover the remaining $24,000 in covered expenses.

The out-of-pocket maximum provides crucial financial protection in situations like the one described above. Without it, you would be responsible for paying the full $7,600, which could place a significant strain on your finances. This underscores the importance of understanding and considering the out-of-pocket maximum when choosing a health insurance plan. It acts as a safety net, preventing potentially devastating medical debt.

Beyond the financial benefits, the out-of-pocket maximum can also provide peace of mind. Knowing that there is a limit to your potential healthcare expenses can reduce stress and anxiety, allowing you to focus on your health and well-being without the constant worry of mounting medical bills. This psychological benefit is often overlooked but is a significant advantage of having a health insurance plan with a reasonable out-of-pocket maximum.

When comparing different health insurance plans, pay close attention to the out-of-pocket maximum, deductible, co-pays, and co-insurance. Use these factors to calculate your potential out-of-pocket expenses under different scenarios. Consider your anticipated healthcare needs and choose a plan that offers the best balance between premium costs and potential out-of-pocket expenses. Tools and resources available online can help you compare plans and estimate your costs.

It’s also crucial to understand the difference between individual and family out-of-pocket maximums. An individual out-of-pocket maximum applies to each individual covered under the plan. A family out-of-pocket maximum applies to the entire family. In some plans, each individual within the family must meet their individual out-of-pocket maximum before the family maximum is met. In other plans, the family maximum is met when the combined out-of-pocket expenses of all family members reach the limit, regardless of whether individual maximums have been met. Clarify these details with your insurance provider to avoid confusion.

Furthermore, be aware that some plans may have separate out-of-pocket maximums for specific types of services, such as prescription drugs or mental health care. These separate maximums can affect your overall healthcare costs, so it’s essential to review your policy carefully and understand any limitations or restrictions. Don’t hesitate to contact your insurance company directly to ask questions and clarify any uncertainties.

The out-of-pocket maximum is a critical component of your health insurance plan, offering crucial financial protection against high medical costs. By understanding how it works and how it interacts with other insurance terms, you can make informed decisions about your healthcare coverage and protect your financial well-being. Take the time to review your policy, compare different plans, and ask questions to ensure you have the coverage that best meets your needs and budget.

Ultimately, understanding your out-of-pocket maximum empowers you to be a more informed and proactive healthcare consumer. It allows you to plan for potential medical expenses, budget accordingly, and make informed decisions about your healthcare treatment. By taking the time to understand this important concept, you can protect yourself and your family from the potentially devastating financial consequences of unexpected medical bills. This knowledge is an investment in your financial security and peace of mind.

Finally, remember that insurance policies can be complex and vary significantly. This article provides general information about out-of-pocket maximums, but it is not a substitute for professional advice. Always consult with your insurance provider or a qualified financial advisor to discuss your specific circumstances and make informed decisions about your healthcare coverage. Taking the initiative to understand your insurance plan is a crucial step towards managing your healthcare costs effectively and protecting your financial future.

FAQs About Out-of-Pocket Maximums:

1. What happens after I reach my out-of-pocket maximum?

Once you reach your out-of-pocket maximum for the plan year, your insurance company will pay 100% of the cost of covered healthcare services for the remainder of that year. You will no longer be responsible for co-pays, co-insurance, or deductible payments for covered services.

2. Does my premium count towards my out-of-pocket maximum?

No, your monthly insurance premiums do not count towards your out-of-pocket maximum. The out-of-pocket maximum only applies to the costs of covered healthcare services that you pay, such as deductibles, co-pays, and co-insurance.

3. What if I have out-of-network expenses? Do they count towards my out-of-pocket maximum?

Generally, out-of-network expenses do not count towards your out-of-pocket maximum unless it’s an emergency situation. However, some plans may offer limited out-of-network coverage, in which case those expenses might contribute to your maximum. Check your policy details to confirm.

4. Are there different out-of-pocket maximums for individuals and families?

Yes, most health insurance plans have separate out-of-pocket maximums for individuals and families. The family maximum is typically higher than the individual maximum. Understand how these limits apply to your specific plan to accurately estimate your potential healthcare costs.

5. Where can I find information about my out-of-pocket maximum?

You can find information about your out-of-pocket maximum in your health insurance policy documents, on your insurance company’s website, or by contacting your insurance provider directly. Look for terms like "out-of-pocket maximum," "OOPM," or "maximum out-of-pocket."

Related Article

- Navigating The Insurance Landscape In Yucca Valley: A Comprehensive Guide

- Navigating The Labyrinth: Understanding Insurance 401(k) Plans

- Diving Into The World Of Insurance: Entry-Level Opportunities And How To Seize Them

- Insurance Agent Salary

- Navigating The Digital Gateway: A Comprehensive Guide To Insurance House Login

Thus, we hope this article has provided valuable insight into Decoding the Out-of-Pocket Maximum: Your Shield Against Catastrophic Healthcare Costs. We thank you for your attention to our article. See you in our next article!