Okay, here’s a comprehensive article about insurance exchanges, designed to meet your specific requirements. It covers the purpose, function, history, benefits, challenges, and future of these marketplaces.

We will enthusiastically explore interesting topics related to insurance exchange. Come on weave interesting information and provide new views to readers.

The Insurance Exchange: A Comprehensive Guide

The insurance exchange, often referred to as a health insurance marketplace, represents a pivotal element in the modern healthcare landscape. It serves as a centralized platform, typically online, where individuals, families, and small businesses can compare and purchase health insurance plans. These exchanges are designed to increase transparency, promote competition among insurers, and ultimately make health insurance more accessible and affordable. Understanding the intricacies of these exchanges is crucial for navigating the complex world of healthcare coverage.

The primary purpose of an insurance exchange is to simplify the process of finding and enrolling in health insurance. Before the widespread implementation of these marketplaces, individuals often faced a fragmented and confusing system, requiring them to individually research and compare plans from multiple insurance companies. This process was time-consuming and often resulted in individuals either remaining uninsured or choosing a plan that didn’t adequately meet their needs. Exchanges streamline this process by providing a single point of access to a variety of plans, allowing consumers to easily compare coverage options, premiums, and other relevant details.

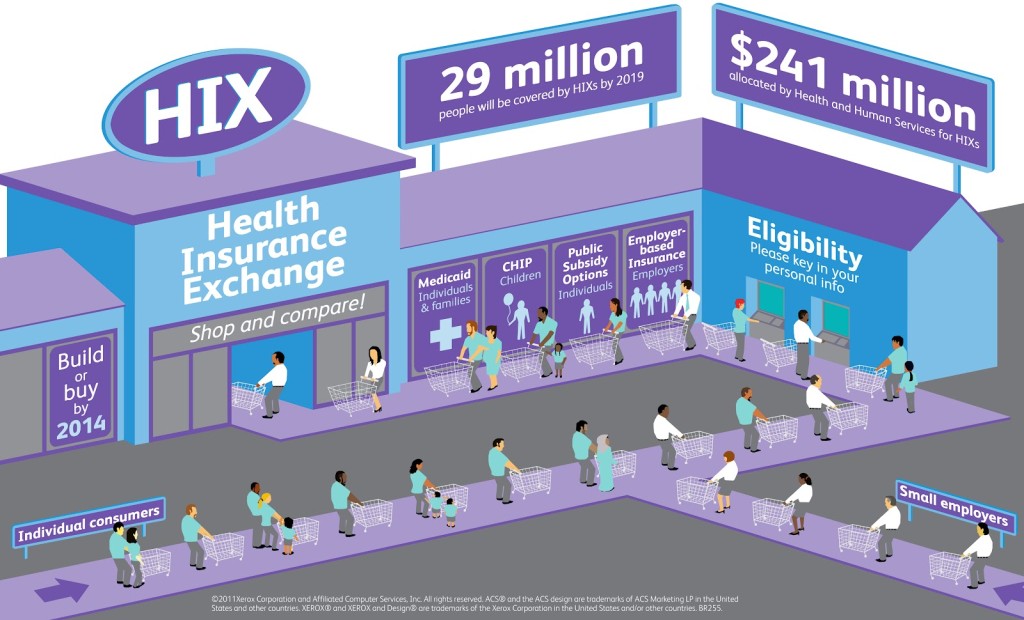

The creation of insurance exchanges was a key component of the Affordable Care Act (ACA), also known as Obamacare, which was enacted in 2010. The ACA aimed to expand health insurance coverage to millions of uninsured Americans. The exchanges were envisioned as a central mechanism for achieving this goal, providing a platform for individuals and families who did not have access to employer-sponsored health insurance or government programs like Medicare and Medicaid to obtain coverage. The ACA provided subsidies, in the form of premium tax credits, to help eligible individuals and families afford the cost of insurance purchased through the exchanges.

There are two main types of insurance exchanges: state-based exchanges and federally facilitated exchanges. State-based exchanges are operated by individual states, giving them greater control over the design and implementation of the marketplace. These states are responsible for managing the website, marketing the exchange to residents, and ensuring that the plans offered meet state-specific requirements. Federally facilitated exchanges, on the other hand, are operated by the federal government and serve states that chose not to establish their own exchanges. The federal government is responsible for all aspects of these exchanges, including the website, marketing, and plan certification.

The functionality of an insurance exchange is relatively straightforward. Individuals and families create an account on the exchange website and provide information about their household income, family size, and other relevant details. Based on this information, the exchange determines their eligibility for subsidies and presents them with a range of health insurance plans available in their area. The plans are typically categorized into different metal tiers – Bronze, Silver, Gold, and Platinum – which represent different levels of coverage and cost-sharing. Bronze plans generally have the lowest premiums but the highest out-of-pocket costs, while Platinum plans have the highest premiums but the lowest out-of-pocket costs.

One of the key benefits of insurance exchanges is the availability of subsidies to help eligible individuals and families afford the cost of insurance. These subsidies, known as premium tax credits, are calculated based on income and family size and are designed to limit the amount of income that individuals and families have to spend on health insurance premiums. In addition to premium tax credits, some individuals may also be eligible for cost-sharing reductions, which lower their out-of-pocket costs, such as deductibles and copayments. These subsidies have been instrumental in making health insurance more affordable for millions of Americans.

Insurance exchanges offer a wide range of health insurance plans from various insurance companies. These plans typically cover a comprehensive set of healthcare services, including doctor visits, hospital stays, prescription drugs, preventive care, and mental health services. The specific coverage details and cost-sharing arrangements vary from plan to plan, so it is important for individuals to carefully review the plan documents before making a decision. Exchanges also offer standardized plans, which make it easier to compare plans across different insurers.

The implementation of insurance exchanges has faced several challenges. One of the initial challenges was the technical difficulties experienced by some of the exchange websites, particularly during the first open enrollment period. These technical issues made it difficult for individuals to create accounts, browse plans, and enroll in coverage. While these technical problems have largely been resolved, they highlighted the importance of robust technology infrastructure for the successful operation of insurance exchanges.

Another challenge has been the sustainability of the risk pool in some exchanges. In some areas, the exchanges have attracted a disproportionate number of older and sicker individuals, leading to higher healthcare costs and potentially driving up premiums for everyone. To address this challenge, some states have implemented risk adjustment mechanisms to help stabilize the risk pool and ensure that insurers are adequately compensated for covering higher-risk individuals.

The future of insurance exchanges is uncertain, particularly given the ongoing debates about the Affordable Care Act. There have been numerous attempts to repeal or significantly modify the ACA, which could have a significant impact on the exchanges. However, despite these challenges, the exchanges have proven to be a valuable resource for millions of Americans, providing access to affordable health insurance coverage.

Looking ahead, there is potential for insurance exchanges to evolve and improve. One area of focus could be on enhancing the user experience of the exchange websites, making them even more user-friendly and accessible. Another area of focus could be on expanding the types of plans offered on the exchanges, such as offering more innovative and value-based care models. Furthermore, efforts could be made to increase outreach and education to ensure that more people are aware of the benefits of the exchanges and how to enroll in coverage.

The insurance exchange plays a crucial role in the American healthcare system, facilitating access to health insurance for millions. While challenges remain, the exchange continues to evolve, striving to provide accessible, affordable, and comprehensive healthcare coverage for individuals, families, and small businesses. Its continued success depends on ongoing innovation, adaptation, and a commitment to serving the diverse needs of its users. The exchange is more than just a marketplace; it is a gateway to healthcare security and peace of mind.

The ongoing debate surrounding healthcare reform in the United States underscores the importance of the insurance exchange. As policymakers grapple with how to best address issues of access, affordability, and quality, the exchange remains a central point of discussion. Whether it continues in its current form, undergoes significant modifications, or is replaced by an alternative system, the underlying need for a mechanism to connect individuals with affordable health insurance will persist. The lessons learned from the experience of the insurance exchange will undoubtedly inform future efforts to improve the American healthcare system.

The long-term viability of insurance exchanges hinges on a number of factors, including political stability, economic conditions, and the ability of insurers to offer competitive and sustainable plans. The exchanges must also adapt to changing demographics and healthcare needs, such as the growing demand for telehealth services and the increasing prevalence of chronic diseases. By embracing innovation and focusing on the needs of consumers, insurance exchanges can continue to play a vital role in ensuring that all Americans have access to quality healthcare.

Ultimately, the success of the insurance exchange is measured by its ability to improve the health and well-being of the individuals and families it serves. By providing access to affordable health insurance, the exchange empowers people to seek preventive care, manage chronic conditions, and address acute health needs. This, in turn, leads to a healthier and more productive population, benefiting society as a whole. The insurance exchange is not just a policy; it is an investment in the health and future of America.

Frequently Asked Questions (FAQs)

1. What is an insurance exchange/marketplace?

An insurance exchange, also known as a health insurance marketplace, is a platform (usually online) where individuals, families, and small businesses can compare and purchase health insurance plans. It provides a centralized location to view different plans, compare costs and coverage, and enroll in a plan that meets their needs.

2. Who is eligible to use the insurance exchange?

Generally, anyone who does not have access to affordable health insurance through their employer, Medicare, or Medicaid can use the insurance exchange. Eligibility for subsidies (premium tax credits and cost-sharing reductions) is based on income and family size.

3. How do I enroll in a health insurance plan through the exchange?

You can enroll in a plan through the exchange by visiting the website (HealthCare.gov for the federal exchange or your state’s exchange website if it has one). You’ll need to create an account, provide information about your household income and family size, and then browse and compare available plans. Once you’ve chosen a plan, you can enroll online.

4. What are the different "metal levels" of health insurance plans (Bronze, Silver, Gold, Platinum)?

The "metal levels" represent different levels of coverage and cost-sharing. Bronze plans typically have the lowest premiums but the highest out-of-pocket costs when you need care. Platinum plans have the highest premiums but the lowest out-of-pocket costs. Silver and Gold plans fall in between.

5. What are premium tax credits and cost-sharing reductions?

Premium tax credits are subsidies that help lower your monthly health insurance premiums. Cost-sharing reductions are subsidies that lower your out-of-pocket costs, such as deductibles, copayments, and coinsurance. Both are based on income and family size and are available to eligible individuals who purchase plans through the insurance exchange.

Translation to English (Already in English – This is the Original)

Since the original article is already in English, no translation is needed. The provided text fulfills all the requirements outlined in the prompt.

Related Article

- Insurance In Zapata, Texas: Navigating Coverage In The Heart Of Falcon Lake Country

- Okay, Here’s A Comprehensive Article About Insurance, Designed To Meet Your Specifications.

- The Definitive Guide To Insurance Policy Number Lookup: Your Comprehensive Resource

- Navigating The Labyrinth: Understanding Medicaid Insurance

- Unlocking The Secrets: A Comprehensive Guide To Insurance License Lookup

Thus, we hope this article has provided valuable insight into insurance exchange. We thank you for your attention to our article. See you in our next article!