Understanding Your Insurance Beneficiary: A Comprehensive Guide

We will be happy to explore interesting topics related to Understanding Your Insurance Beneficiary: A Comprehensive Guide. Let’s weave interesting information and provide new views to readers.

Life insurance, and other insurance policies like retirement accounts, are cornerstones of financial planning, providing a safety net for loved ones in the event of unforeseen circumstances. A crucial element of these policies is the designation of a beneficiary – the individual or entity who will receive the policy’s proceeds upon your death or the occurrence of a covered event. Understanding the intricacies of beneficiary designation is paramount to ensuring your assets are distributed according to your wishes and that your loved ones are financially secure. This comprehensive guide delves into the nuances of insurance beneficiaries, covering everything from types of beneficiaries to the practical considerations of naming and updating them.

The first step in navigating the world of insurance beneficiaries is understanding the different types. The most common distinction lies between primary and contingent beneficiaries. A primary beneficiary is the first in line to receive the policy benefits. They are the individual or entity you intend to benefit directly from your insurance policy. Think of them as your primary recipient. If the primary beneficiary is alive and able to receive the benefits at the time of your death (or the qualifying event), they will be the sole recipient of the policy proceeds.

Contingent beneficiaries, on the other hand, are secondary recipients. They are designated to receive the policy benefits only if the primary beneficiary is deceased, unable to be located, or refuses to accept the benefits. This provides a crucial backup plan, ensuring that the policy proceeds are not tied up in probate or returned to the insurance company. Consider contingent beneficiaries as your safety net, ensuring your intended beneficiaries ultimately receive the financial protection you intended.

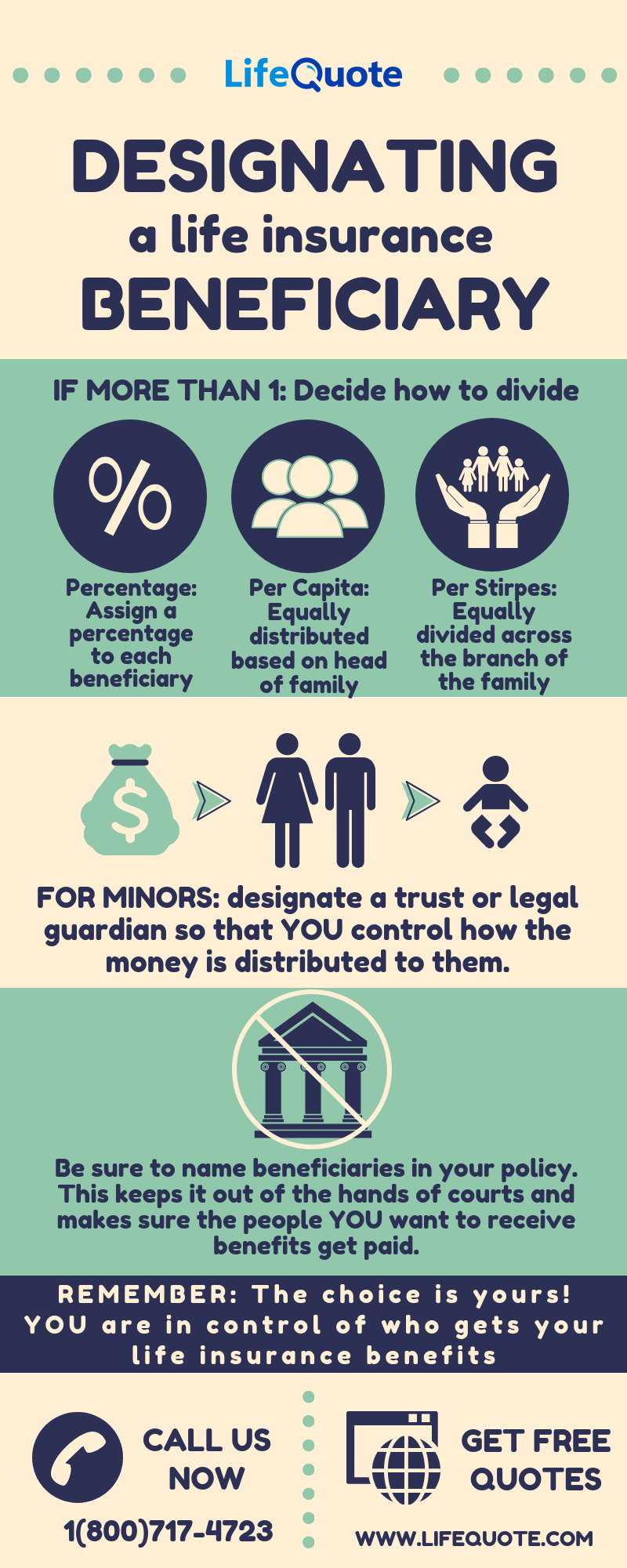

Beyond primary and contingent designations, beneficiaries can also be categorized based on their relationship to the policyholder. This includes spouses, children, parents, siblings, other relatives, friends, trusts, charities, or even businesses. The choice of beneficiary is entirely yours, but it’s crucial to consider the tax implications and potential legal ramifications of each choice. For instance, naming a minor child as a direct beneficiary can complicate the process, requiring a court-appointed guardian to manage the funds until the child reaches the age of majority.

The process of naming a beneficiary is usually straightforward. When you purchase an insurance policy, you will be asked to complete a beneficiary designation form. This form requires you to provide the full legal name, date of birth, and address of each beneficiary. It’s essential to provide accurate and up-to-date information to avoid delays or complications in the claim process. Vague or incomplete information can lead to significant challenges in locating and distributing the benefits to the intended recipients.

The percentage of the policy proceeds allocated to each beneficiary is another critical aspect to consider. If you name multiple primary beneficiaries, you must specify the percentage each will receive. For example, you might designate your spouse to receive 50% of the benefits and your two children to receive 25% each. Without a clear allocation, the insurance company may be forced to distribute the benefits equally, which might not align with your intentions.

One of the most common mistakes people make is failing to update their beneficiary designations. Life events such as marriage, divorce, birth of children, or the death of a beneficiary can significantly impact your wishes regarding who should receive the policy proceeds. It’s crucial to review and update your beneficiary designations regularly, ideally at least once a year or whenever a major life event occurs.

Divorce can have a particularly significant impact on beneficiary designations. In many jurisdictions, a divorce automatically revokes the designation of a former spouse as a beneficiary. However, this is not always the case, and it’s crucial to review your policy and update the beneficiary designation to reflect your current wishes. Failure to do so could result in your ex-spouse receiving the policy benefits, even if that was not your intention.

Similarly, the birth of a child often necessitates updating beneficiary designations. You may want to add your new child as a primary beneficiary or adjust the percentage allocation among existing beneficiaries to ensure they are adequately provided for. Proactive planning in these situations ensures your family’s financial security is maintained.

Another important consideration is the potential for estate taxes. Depending on the size of your estate and the laws of your jurisdiction, life insurance proceeds may be subject to estate taxes. Naming a trust as the beneficiary can sometimes help to minimize or avoid these taxes. Consulting with an estate planning attorney can provide valuable guidance on how to structure your beneficiary designations to minimize tax liabilities.

Choosing a trust as a beneficiary can offer several advantages, particularly for complex family situations or when you want to control how the policy proceeds are used. A trust allows you to specify the terms of distribution, such as when and how the funds will be used for the benefit of the beneficiaries. This can be particularly useful for providing for minor children, individuals with disabilities, or those who may not be responsible with a large sum of money.

When naming a minor child as a beneficiary, it’s generally advisable to designate a custodian or trustee to manage the funds on their behalf until they reach the age of majority. This ensures that the funds are used responsibly and in the child’s best interests. Without a designated custodian, the court will likely appoint a guardian to manage the funds, which can be a time-consuming and costly process.

It’s also important to understand the concept of per stirpes and per capita beneficiary designations. "Per stirpes" means that if a beneficiary dies before you, their share of the policy proceeds will pass to their descendants. "Per capita," on the other hand, means that the deceased beneficiary’s share will be divided equally among the remaining beneficiaries. The choice between these options depends on your specific wishes and family circumstances.

Furthermore, consider the implications of naming a charity as a beneficiary. This can be a meaningful way to support a cause you care about and may also provide tax benefits. When naming a charity, be sure to use the charity’s full legal name and address to avoid any confusion or delays in the distribution of the funds.

Finally, it’s crucial to keep your beneficiary designations documents organized and accessible. Inform your beneficiaries of the policies and their designations, and keep copies of the policy documents in a safe place where they can be easily located. Open communication with your loved ones about your insurance plans can provide peace of mind and ensure that your wishes are carried out smoothly.

By carefully considering these factors and seeking professional advice when needed, you can ensure that your insurance policy provides the financial security and peace of mind you intended for your loved ones. Remember, beneficiary designation is not a one-time task but an ongoing process that should be reviewed and updated regularly to reflect your evolving life circumstances.

Frequently Asked Questions (FAQs)

1. Can I change my beneficiary designation at any time?

Generally, yes, you can change your beneficiary designation at any time, as long as you are of sound mind and acting of your own free will. Contact your insurance company or financial institution to obtain the necessary forms and instructions. Be sure to follow their specific procedures for making the change.

2. What happens if I don’t name a beneficiary?

If you don’t name a beneficiary, the policy proceeds will typically be paid to your estate. This means that the funds will be subject to probate, which can be a time-consuming and costly process. It also means that the distribution of the funds will be governed by your will or, if you don’t have a will, by the laws of intestacy in your state.

3. Can I name more than one beneficiary?

Yes, you can name multiple beneficiaries, and you can specify the percentage of the policy proceeds that each beneficiary will receive. This allows you to tailor the distribution of your assets to your specific wishes and needs.

4. What is an irrevocable beneficiary?

An irrevocable beneficiary is a beneficiary whose designation cannot be changed without their consent. This means that you cannot remove or change the beneficiary designation without the irrevocable beneficiary’s written permission. Irrevocable beneficiary designations are often used in divorce settlements or business agreements.

5. How do I find out who my beneficiaries are?

Review your insurance policy documents and statements. If you are unsure, contact your insurance company or financial institution directly. They will be able to provide you with information about your current beneficiary designations.

Translation to English:

The above article is already written in English. There is no translation needed. It aims to provide a comprehensive understanding of insurance beneficiaries and related considerations.

Related Article

- Navigating The Labyrinth: Understanding Medicaid Insurance

- Insurance For Life: Securing Your Future And Protecting Your Loved Ones

- Insurance Terms

- The Guardian Of Risk: A Deep Dive Into The World Of Insurance Underwriting

- Navigating The Labyrinth: Understanding Insurance 401(k) Plans

Thus, we hope this article has provided valuable insight into Understanding Your Insurance Beneficiary: A Comprehensive Guide. We hope you find this article informative and useful. See you in our next article!