Insurance 110: A Comprehensive Guide to Understanding the Basics

We will enthusiastically explore interesting topics related to Insurance 110: A Comprehensive Guide to Understanding the Basics. Let’s weave interesting information and provide new views to readers.

Insurance. The word itself can evoke feelings ranging from mild confusion to outright dread. It’s often seen as a necessary evil, a cost we endure for something we hope we never need. But at its core, insurance is a powerful tool that provides financial security and peace of mind in the face of unexpected events. This guide, Insurance 110, aims to demystify the basics of insurance, providing a foundational understanding of its principles, types, and importance in modern life. We’ll explore the fundamental concepts that underpin the insurance industry, empowering you to make informed decisions about protecting yourself, your family, and your assets.

At its most basic, insurance is a contract, a legally binding agreement between an insurer and an insured. The insurer, typically a large company, agrees to compensate the insured for specific losses or damages in exchange for a payment, known as a premium. This premium represents the price of the insurance coverage, calculated based on the perceived risk of the insured experiencing a covered event. The higher the risk, the higher the premium, and vice versa. This risk assessment is a crucial part of the insurance process, involving careful consideration of factors like age, health, location, and lifestyle.

The principle of risk pooling is fundamental to how insurance works. Insurers collect premiums from a large number of individuals, creating a pool of funds. This pool is then used to pay out claims to those who experience a covered loss. By spreading the risk across a large group, the financial burden of an individual loss is shared, making it manageable for everyone involved. Without this risk pooling mechanism, individuals would be solely responsible for bearing the full cost of potentially devastating events, which could lead to financial ruin.

One of the most important concepts in insurance is the "insurable interest." This means that the person taking out the insurance policy must have a financial stake in the item or person being insured. You can’t, for example, insure your neighbor’s house simply because you like the look of it. You must demonstrate that you would suffer a financial loss if the insured item were damaged or destroyed, or if the insured person were to experience a covered event. This principle prevents insurance from being used for gambling or speculative purposes and ensures that there is a legitimate reason for the coverage.

Another key element is the concept of "indemnity." Indemnity aims to restore the insured to the financial position they were in before the loss occurred, but not to profit from the loss. This means that the insurance payout should cover the actual cost of the damage or loss, less any deductible. The goal is to make the insured whole, not to provide a windfall. This principle prevents insurance from being used as a means of enrichment and helps to control insurance costs by preventing fraudulent claims.

There are numerous types of insurance available, each designed to protect against different kinds of risks. Some of the most common types include health insurance, life insurance, auto insurance, homeowners insurance, and renters insurance. Health insurance covers medical expenses incurred due to illness or injury. Life insurance provides a financial benefit to beneficiaries upon the death of the insured. Auto insurance protects against financial losses resulting from car accidents. Homeowners insurance covers damage to a home and its contents, as well as liability for injuries that occur on the property. Renters insurance covers a renter’s personal belongings and liability within a rented property.

Health insurance is crucial for managing the potentially crippling costs of medical care. It can cover doctor visits, hospital stays, prescription drugs, and other medical services. Without health insurance, a single serious illness or injury could lead to overwhelming medical debt. There are various types of health insurance plans, including HMOs, PPOs, and high-deductible health plans, each with its own set of benefits and costs. Choosing the right health insurance plan depends on individual needs and circumstances.

Life insurance provides financial protection for your loved ones in the event of your death. It can help cover funeral expenses, pay off debts, and provide ongoing income for your family. There are two main types of life insurance: term life insurance, which provides coverage for a specific period of time, and permanent life insurance, which provides coverage for your entire life and also accumulates cash value. The amount of life insurance you need depends on factors such as your income, debts, and the number of dependents you have.

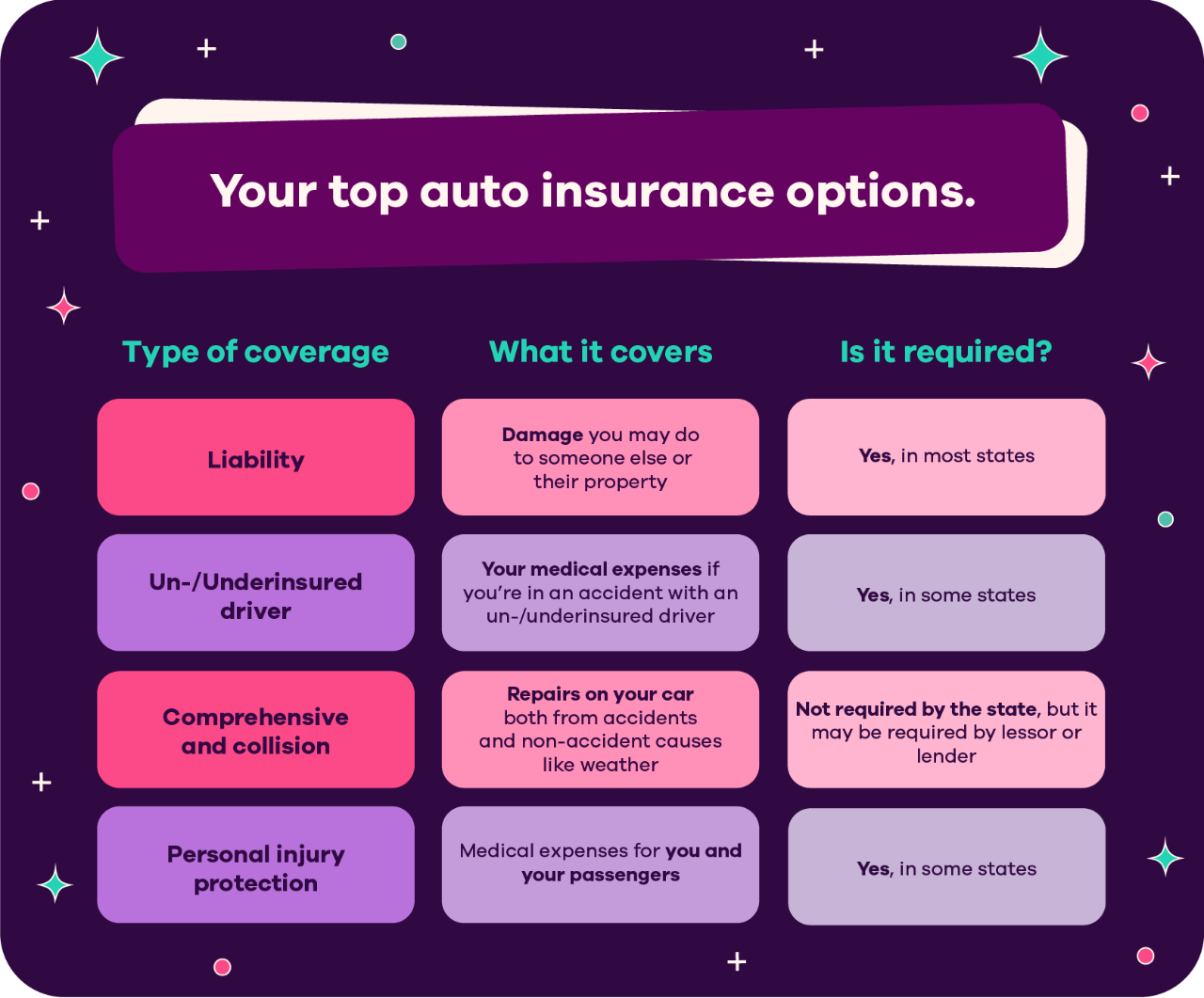

Auto insurance is legally required in most states and protects you financially if you cause an accident or if your car is damaged or stolen. It can cover the cost of repairing or replacing your vehicle, as well as medical expenses and legal fees if you are found liable for causing an accident. There are different types of auto insurance coverage, including liability coverage, collision coverage, and comprehensive coverage. The amount of coverage you need depends on your driving habits, the value of your car, and your financial situation.

Homeowners insurance protects your home and its contents from damage caused by events such as fire, windstorms, theft, and vandalism. It also provides liability coverage if someone is injured on your property. The amount of homeowners insurance you need depends on the replacement cost of your home and the value of your personal belongings. It’s important to review your homeowners insurance policy regularly to ensure that you have adequate coverage.

![]()

Renters insurance is similar to homeowners insurance, but it covers your personal belongings and liability within a rented property. It’s an affordable way to protect yourself from financial losses due to theft, fire, or other covered events. Even if your landlord has insurance, it typically only covers the building itself, not your personal belongings. Renters insurance is often required by landlords as a condition of the lease.

Understanding the terms and conditions of your insurance policies is crucial. Pay close attention to the exclusions, which are specific events or circumstances that are not covered by the policy. Also, be aware of the deductibles, which are the amount you must pay out-of-pocket before your insurance coverage kicks in. Regularly review your policies and make sure they still meet your needs as your circumstances change.

Filing a claim is a straightforward process, but it’s important to follow the insurer’s instructions carefully. Typically, you’ll need to notify the insurer as soon as possible after the loss occurs, provide documentation of the damage or loss, and cooperate with the insurer’s investigation. Be honest and accurate in your claim, as fraudulent claims can result in denial of coverage and even legal penalties. Keep records of all communication with the insurer and retain copies of all documents submitted.

Choosing the right insurance policies can be overwhelming, but it’s essential for protecting your financial well-being. Consider your individual needs and circumstances, and shop around for the best coverage at the most affordable price. Compare quotes from different insurers and read reviews to get a sense of their customer service and claims handling. Don’t be afraid to ask questions and seek advice from insurance professionals.

In conclusion, insurance is an indispensable tool for managing risk and protecting yourself from financial hardship. By understanding the basic principles of insurance, the different types of coverage available, and the terms and conditions of your policies, you can make informed decisions about protecting yourself, your family, and your assets. While it may seem complex at times, the peace of mind that insurance provides is well worth the effort. It’s not just about paying premiums; it’s about investing in your future security and well-being.

Frequently Asked Questions (FAQs)

1. What is a deductible, and how does it affect my insurance premiums?

A deductible is the amount of money you pay out-of-pocket before your insurance coverage kicks in. For example, if you have a $500 deductible and file a claim for $1,000, you will pay $500, and the insurance company will pay the remaining $500. Generally, the higher your deductible, the lower your insurance premiums will be, and vice versa. This is because you are taking on more of the risk yourself. Choosing the right deductible involves balancing the cost of premiums with the potential out-of-pocket expenses in the event of a claim.

2. What is the difference between term life insurance and whole life insurance?

Term life insurance provides coverage for a specific period of time, such as 10, 20, or 30 years. If you die within the term, your beneficiaries will receive a death benefit. If you outlive the term, the coverage expires. Whole life insurance, on the other hand, provides coverage for your entire life and also accumulates cash value over time. This cash value can be borrowed against or withdrawn, making it a more flexible option. Term life insurance is typically less expensive than whole life insurance, but it does not offer the cash value component.

3. What does "liability coverage" mean in auto insurance?

Liability coverage in auto insurance protects you financially if you are found responsible for causing an accident that results in injuries or property damage to others. It covers the other party’s medical expenses, car repairs, and other related costs, up to the limits of your policy. Liability coverage is essential because it can protect you from potentially devastating financial losses if you are sued for damages. Most states require drivers to carry a minimum amount of liability coverage.

4. What are some common exclusions in homeowners insurance policies?

Common exclusions in homeowners insurance policies include damage caused by earthquakes, floods, landslides, and acts of war. These events are typically considered to be too catastrophic or unpredictable to be covered under a standard homeowners policy. You may need to purchase separate insurance policies, such as earthquake insurance or flood insurance, to protect against these risks. It’s important to carefully review your policy to understand what is and is not covered.

5. How can I lower my insurance premiums?

There are several ways to potentially lower your insurance premiums. You can increase your deductible, shop around for quotes from different insurers, bundle your insurance policies (e.g., auto and homeowners), maintain a good credit score, and take advantage of discounts offered by insurers (e.g., safe driver discount, home security system discount). Reviewing your insurance needs annually and making adjustments as necessary can also help you save money.

Related Article

- Insurance Queen

- Navigating The Labyrinth: Understanding Medicaid Insurance

- Navigating The World Of Dental Insurance: A Comprehensive Guide

- Insurance Eob

- Insurance For Life: Securing Your Future And Protecting Your Loved Ones

Thus, we hope this article has provided valuable insight into Insurance 110: A Comprehensive Guide to Understanding the Basics. We thank you for taking the time to read this article. See you in our next article!