Navigating the Labyrinth: A Comprehensive Guide to Insurance Enrollment Periods

We will enthusiastically explore interesting topics related to Navigating the Labyrinth: A Comprehensive Guide to Insurance Enrollment Periods. Come on weave interesting information and provide new views to readers.

Insurance. The very word can evoke a mix of feelings, from relief and security to confusion and frustration. For many, it’s a necessary evil, a financial safety net that protects us from the unpredictable storms of life. But understanding the intricacies of insurance, particularly the all-important enrollment periods, can feel like navigating a labyrinth. This comprehensive guide aims to demystify the process, providing you with the knowledge and confidence to make informed decisions about your healthcare and other insurance needs.

The concept of an enrollment period is fundamentally about managing risk and ensuring the stability of the insurance pool. Without designated enrollment periods, individuals might only seek coverage when they anticipate needing it, leading to a pool of insured individuals skewed towards those with pre-existing conditions or imminent health concerns. This “adverse selection” can drive up premiums for everyone, making insurance less affordable and accessible. Therefore, enrollment periods serve as a crucial mechanism to balance the risk pool and maintain the financial viability of insurance plans.

The cornerstone of understanding enrollment periods lies in recognizing that they are not universal. Different types of insurance have their own specific enrollment windows, each with its own rules and regulations. For instance, employer-sponsored health insurance typically has an annual open enrollment period, usually in the fall. This is the time when employees can review their current coverage, compare different plan options, and make changes to their benefits for the upcoming year. Miss this window, and you generally have to wait until the next open enrollment unless you experience a qualifying life event.

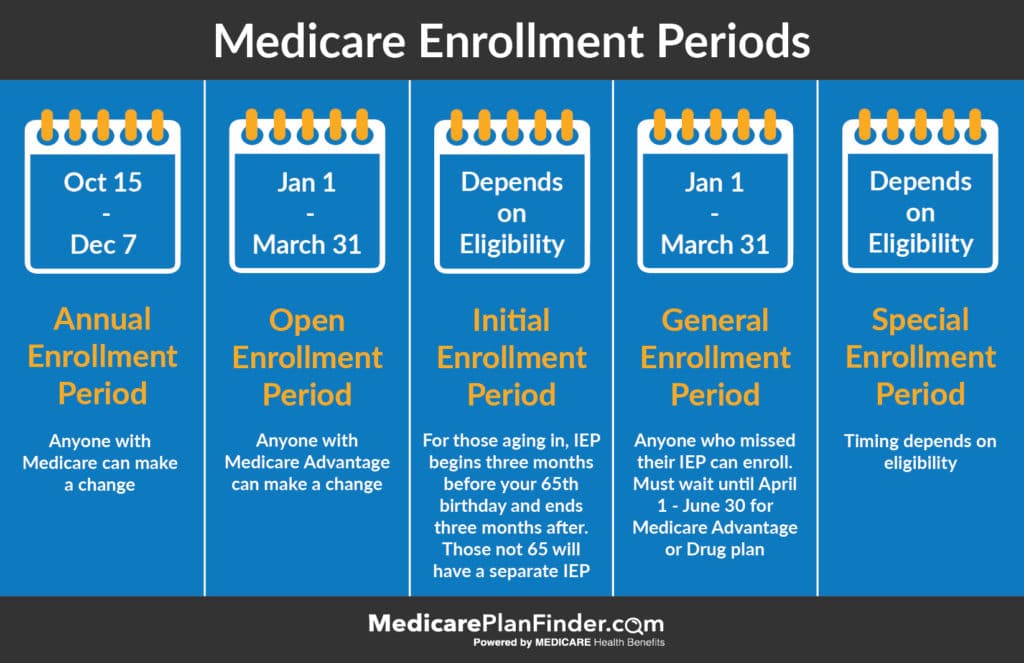

On the other hand, Medicare, the federal health insurance program for individuals 65 and older and certain younger people with disabilities, has its own set of enrollment periods. The Initial Enrollment Period (IEP) is a 7-month window surrounding your 65th birthday, allowing you to sign up for Medicare Part A (hospital insurance) and Part B (medical insurance). There’s also the General Enrollment Period (GEP) from January 1st to March 31st each year for those who didn’t enroll during their IEP. Furthermore, the Annual Enrollment Period (AEP), also known as Medicare Open Enrollment, runs from October 15th to December 7th, allowing beneficiaries to make changes to their Medicare Advantage or Part D prescription drug plans.

The Affordable Care Act (ACA), also known as Obamacare, established the Health Insurance Marketplace, offering subsidized health insurance plans to individuals and families who don’t have access to employer-sponsored coverage. The Health Insurance Marketplace typically has an annual open enrollment period that runs from November 1st to January 15th in most states. During this period, individuals can enroll in a new health plan, renew their existing coverage, or switch to a different plan. Understanding the specific dates for your state is crucial, as some states may have extended or shortened enrollment periods.

Beyond health insurance, other types of insurance, such as life insurance, disability insurance, and even property insurance, may also have specific enrollment periods or underwriting guidelines that affect when you can obtain coverage. While life insurance policies can generally be purchased year-round, the cost of premiums can be significantly affected by your age and health. Disability insurance, which protects your income if you become unable to work due to illness or injury, often has stricter underwriting requirements and may require a medical exam before coverage is approved.

One of the most crucial aspects of navigating enrollment periods is understanding the concept of “qualifying life events.” These are significant changes in your life circumstances that allow you to enroll in or modify your insurance coverage outside of the standard open enrollment periods. Qualifying life events can include marriage, divorce, the birth or adoption of a child, loss of employer-sponsored coverage, a change in residence, or other significant life changes that impact your insurance needs.

If you experience a qualifying life event, you typically have a limited time frame, often 30 to 60 days, to enroll in or modify your insurance coverage. It’s essential to act quickly and provide the necessary documentation to verify your qualifying life event. Failure to do so within the specified timeframe may result in having to wait until the next open enrollment period to obtain coverage. This can leave you vulnerable to financial risks if you experience an unexpected illness or injury during the interim.

Choosing the right insurance plan can feel overwhelming, especially with the myriad of options available. It’s crucial to carefully consider your individual needs, budget, and risk tolerance when making your decision. Factors to consider include the monthly premium, deductible, co-pays, co-insurance, and the plan’s network of doctors and hospitals. If you have specific healthcare needs or prefer to see certain providers, it’s essential to ensure that the plan covers those services and providers.

Don’t hesitate to seek professional guidance when navigating the complexities of insurance enrollment. Insurance brokers and agents can provide valuable assistance in understanding your options, comparing different plans, and enrolling in the coverage that best meets your needs. They can also help you understand the fine print of your policy and answer any questions you may have. Many insurance companies also offer customer service representatives who can assist you with enrollment and answer your questions.

![]()

Furthermore, numerous online resources are available to help you research and compare insurance plans. The Health Insurance Marketplace website provides a wealth of information about ACA-compliant health plans, including plan details, premiums, and cost-sharing information. Medicare.gov offers comprehensive information about Medicare coverage, enrollment periods, and available plans. Utilizing these resources can empower you to make informed decisions about your insurance coverage.

Understanding the nuances of insurance enrollment periods is not merely a matter of ticking boxes; it’s about safeguarding your financial well-being and ensuring access to necessary healthcare services. Taking the time to research your options, understand your rights, and seek professional guidance can make a significant difference in your ability to navigate the insurance landscape with confidence and peace of mind. Don’t wait until the last minute to enroll; start planning early and make sure you have the coverage you need to protect yourself and your loved ones.

In conclusion, mastering the intricacies of insurance enrollment periods requires a proactive and informed approach. From understanding the different types of enrollment periods to recognizing qualifying life events and seeking professional guidance, each step plays a crucial role in securing the right coverage for your specific needs. By embracing this comprehensive understanding, you can confidently navigate the insurance landscape and safeguard your future. Remember, insurance is not just a financial obligation; it’s an investment in your health, security, and peace of mind. So, take the time to learn, explore your options, and make informed decisions that will protect you and your family for years to come.

The process of enrolling in an insurance plan can be complex, but it’s ultimately about empowering yourself to make informed decisions about your health and financial security. By taking the time to understand the different enrollment periods, qualifying life events, and plan options, you can navigate the insurance landscape with confidence and ensure that you have the coverage you need to protect yourself and your loved ones.

Remember to compare different plans carefully, considering factors such as premiums, deductibles, co-pays, and network coverage. Don’t hesitate to seek professional guidance from insurance brokers or agents who can help you understand your options and enroll in the plan that best meets your needs. And most importantly, don’t wait until the last minute to enroll; start planning early and make sure you have the coverage you need when you need it.

By taking a proactive and informed approach to insurance enrollment, you can safeguard your financial well-being and ensure access to the healthcare services you need to live a healthy and fulfilling life. Insurance is not just a financial obligation; it’s an investment in your future and the future of your loved ones. So, take the time to learn, explore your options, and make informed decisions that will protect you for years to come.

Finally, always keep your insurance documents organized and readily accessible. This will make it easier to access your coverage information when you need it and ensure that you are always aware of your rights and responsibilities as an insured individual. By staying informed and organized, you can make the most of your insurance coverage and protect yourself from unexpected financial burdens.

Frequently Asked Questions (FAQs)

1. What happens if I miss the open enrollment period for my employer-sponsored health insurance?

If you miss the open enrollment period for your employer-sponsored health insurance, you generally have to wait until the next open enrollment period to enroll in coverage or make changes to your existing plan. However, if you experience a qualifying life event, such as marriage, divorce, the birth of a child, or loss of other coverage, you may be eligible for a special enrollment period.

2. What is a qualifying life event and how does it affect my ability to enroll in insurance?

A qualifying life event is a significant change in your life circumstances that allows you to enroll in or modify your insurance coverage outside of the standard open enrollment periods. Common qualifying life events include marriage, divorce, the birth or adoption of a child, loss of employer-sponsored coverage, a change in residence, or other significant life changes that impact your insurance needs. If you experience a qualifying life event, you typically have a limited time frame, often 30 to 60 days, to enroll in or modify your insurance coverage.

3. How do I choose the right health insurance plan for my needs?

Choosing the right health insurance plan requires careful consideration of your individual needs, budget, and risk tolerance. Factors to consider include the monthly premium, deductible, co-pays, co-insurance, and the plan’s network of doctors and hospitals. If you have specific healthcare needs or prefer to see certain providers, it’s essential to ensure that the plan covers those services and providers. Don’t hesitate to seek professional guidance from insurance brokers or agents who can help you understand your options and enroll in the plan that best meets your needs.

4. What is the difference between Medicare’s Initial Enrollment Period (IEP) and Annual Enrollment Period (AEP)?

Medicare’s Initial Enrollment Period (IEP) is a 7-month window surrounding your 65th birthday, allowing you to sign up for Medicare Part A (hospital insurance) and Part B (medical insurance). The Annual Enrollment Period (AEP), also known as Medicare Open Enrollment, runs from October 15th to December 7th each year, allowing beneficiaries to make changes to their Medicare Advantage or Part D prescription drug plans.

5. Where can I find more information about insurance enrollment periods and available plans?

You can find more information about insurance enrollment periods and available plans from various sources, including the Health Insurance Marketplace website (healthcare.gov), Medicare.gov, your employer’s benefits department, and insurance brokers or agents. These resources can provide valuable information about plan details, premiums, cost-sharing information, and enrollment deadlines.

Translation to English (The above article is already in English, so this section is redundant. However, if the original was in another language, this is where the English translation would go.)

Since the provided text is already in English, a translation is not necessary.

Related Article

- Insurance Warehouse

- The Guardian Of Risk: A Deep Dive Into The World Of Insurance Underwriting

- Navigating The Healthcare Maze: A Comprehensive Look At Health Insurance Companies

- Diving Into The World Of Insurance: Entry-Level Opportunities And How To Seize Them

- Decoding The Labyrinth: A Comprehensive Guide To Insurance Code 743

Thus, we hope this article has provided valuable insight into Navigating the Labyrinth: A Comprehensive Guide to Insurance Enrollment Periods. We thank you for taking the time to read this article. See you in our next article!